Author: Eric Bernstein

Author: Eric BernsteinPublished:

|

|

Our LendFriend Learning Center now has over 250 articles to help homebuyers buy with confidence. Check out our top articles of the week at the bottom of this email.

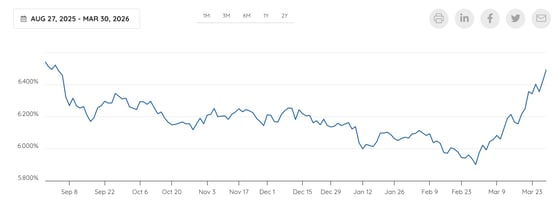

Inflation Is Starting to Pop Up Around the World

Global inflation is quietly making a comeback, and for homebuyers and homeowners interested in refinancing, it's worth paying attention to.

German consumer prices jumped to 2.8% year-over-year in March, the highest reading in more than a year, driven largely by the ongoing Iran war pushing energy costs higher. Spain saw inflation hit 3.3%, and the euro zone as a whole is expected to clock in at 2.6%, which is the highest since July 2024.

Money markets are already pricing in an ECB rate hike as soon as April, with up to three hikes expected over the course of the year.

Why does this matter for U.S. mortgage rates? Global inflation doesn't stay global for long. When energy prices rise overseas, they eventually flow through to American consumers too — in the form of higher gas prices, shipping costs, and goods prices. That puts upward pressure on U.S. inflation, which keeps the Fed cautious about cutting rates, and ultimately keeps mortgage rates elevated longer than buyers would like.

The bottom line: the Iran conflict is becoming a meaningful wildcard for anyone watching rates. If the war drags on and energy prices keep climbing, the window for rate cuts, here and abroad, could get smaller before it gets bigger.

Rate Cuts Aren't the Only Way Mortgage Rates Come DownMost people think the only path to lower mortgage rates is the Fed cutting rates. But there's another way that doesn't get enough attention: the Fed's balance sheet.

The Labor Market Is Holding Up — For Now

Despite all the uncertainty around tariffs and the Iran war, the labor market is holding steady. Initial jobless claims came in at 210,000 last week — near the lowest levels of the past year — and continuing claims dropped to their lowest point since May 2024. Layoffs remain low. The catch: long-term unemployment is quietly rising, and if the energy shock starts hitting hiring, that story could change fast. We'll get a better picture of the labor market this week as reporting rolls in.

What to expect this week?

Tuesday brings job openings (expected at 7.0 million) and consumer confidence (expected at 88.0, down from 91.2) — an early read on whether households and employers are starting to pull back.

|

This Week's Top Learning Center Articles

-

Self-Employed Cash-Out Refinance: Qualify Using A Bank Statement Loan

- Mortgage Refinancing Options in New Jersey for Business Owners

I'm always here to help so if you have any questions or just want to learn more, schedule a call or connect with me here.

.png?width=1200&height=244&name=Homebuyer%20Tools%20Header%20(10).png)