Author: Eric Bernstein

Author: Eric BernsteinPublished:

DSCR loans have become one of the most practical financing options for real estate investors targeting high-value properties in competitive markets like Florida, Texas, and California.

Unlike traditional mortgages, DSCR (Debt Service Coverage Ratio) loans focus on the income-generating ability of the property, not the borrower’s personal income. This makes them attractive for investors scaling portfolios or purchasing luxury rental properties.

Before applying, it’s important to understand both the pros and cons of DSCR loans, especially when dealing with high-value investment properties. However, DSCR guidelines vary depending on lender overlays, property type, and loan size

What Is a DSCR Loan?

A DSCR loan is a type of real estate investment loan where approval is based on the property’s ability to generate enough rental income to cover its debt obligations.

Instead of verifying W-2s, tax returns, or employment history, lenders evaluate:

- Rental income from the property

- Mortgage payment (PITI: principal, interest, taxes, insurance)

- DSCR ratio (income vs debt obligation)

A DSCR ratio of 1.0 means break-even, and most lenders prefer:

- 0.75 – 1.25+ (minimum acceptable range)

- Higher ratios = stronger loan approval chances

How DSCR Loans Work

The formula is simple:

DSCR = Net Operating Income (NOI) ÷ Annual Mortgage Payments

- If DSCR > 1 → Property generates more income than debt payments

- If DSCR < 1 → Property does not fully cover loan payments.

However, DSCR loans are more flexible than many investors realize. Some lenders can approve loans with a DSCR as low as 0.75, but this comes with trade-offs.

For example, if a property brings in $60,000 in annual net income and your mortgage payments are $48,000, your DSCR is 1.25. It is a strong number in most markets.

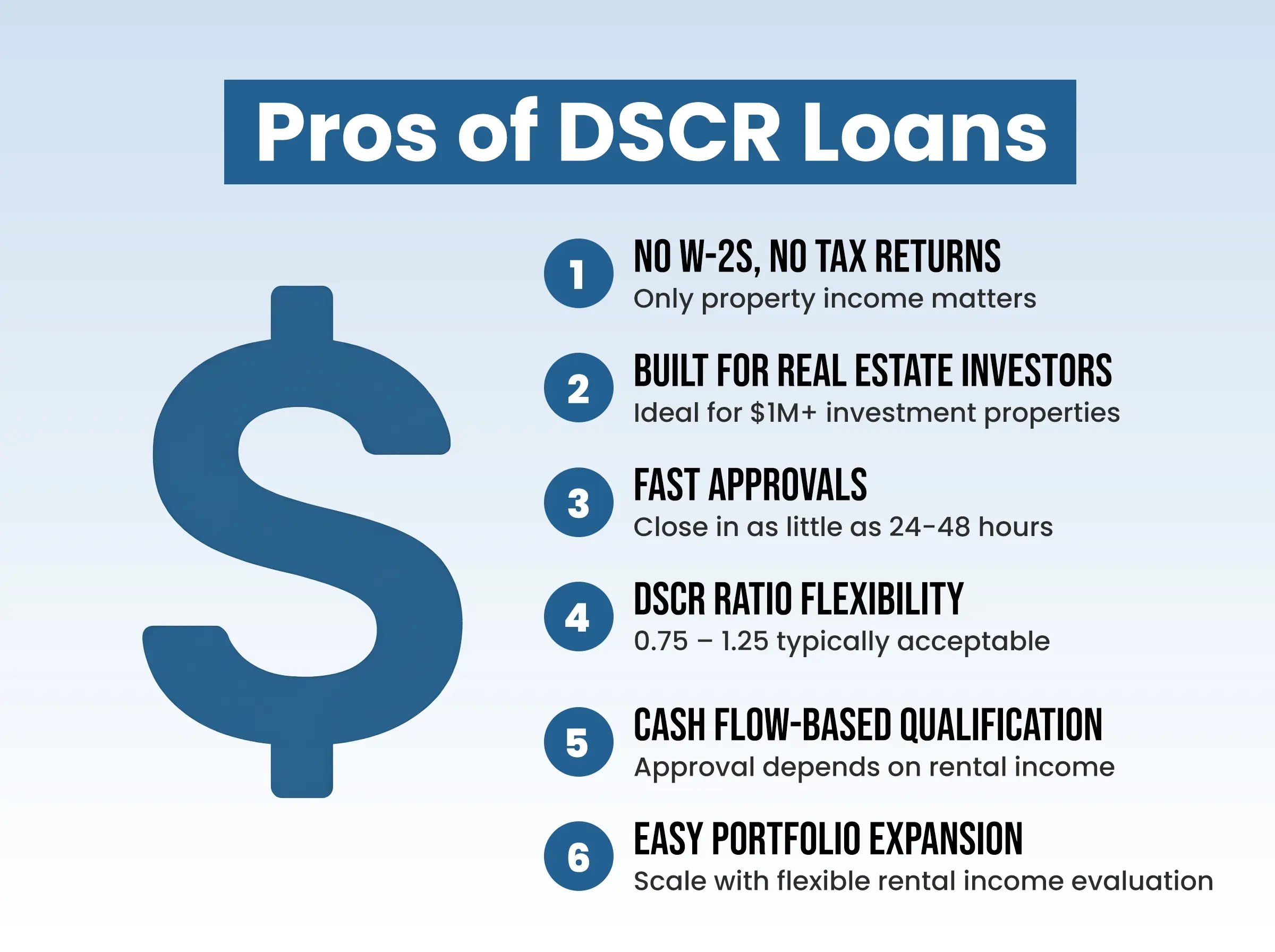

Pros of DSCR Loans

1. No Personal Income Verification Required

One of the biggest advantages of DSCR loans is that qualification is based on the property’s income, not the borrower’s personal earnings. Investors are not required to submit

- W-2 income

- Tax returns

- Employment verification

This is especially useful for:

- Real estate investors with multiple properties

- Self-employed borrowers

- High-net-worth individuals with complex income structures

2. Strong Fit for High-Cash-Flow Investment Properties

In markets of Florida and Texas, where rental demand is strong, DSCR loans allow investors to leverage property cash flow rather than personal income.

If the property performs well, approval becomes significantly easier, even for multi-million-dollar assets. Investors can leverage the property’s performance to qualify, rather than relying on traditional income metrics that may not reflect real investment strength.

3. Ideal for Scaling in Florida, Texas & California

DSCR financing is useful in major U.S. investment markets such as Florida, Texas, and California, where rental demand and property appreciation potential remain strong.

- Florida offers strong short-term and vacation rental demand

- Texas provides consistent population growth and stable rental markets

- California delivers long-term appreciation despite higher entry costs

Because DSCR loans do not rely on personal income limits, investors can scale their portfolios more efficiently across these high-opportunity markets without being restricted by traditional lending constraints.

4. Faster Approval Compared to Traditional Loans

Because DSCR loans skip income documentation, underwriting is typically faster.

This can help investors:

- Close deals quickly

- Compete in competitive real estate markets

- Secure properties before other buyers

This faster approval process can be a major advantage in competitive real estate markets, where speed often determines whether an investor successfully secures a property or loses it to another buyer. It also helps reduce documentation delays and simplifies the overall lending experience.

5. Flexible Underwriting Based on Rental Income

Approval is tied to the property’s performance, not the borrower’s financial background.

It provides:

- More flexibility for experienced investors

- Easier qualification for non-traditional income earners

- Financing based on investment logic rather than personal salary

This makes it easier for investors with non-traditional financial profiles to qualify, provided the property demonstrates strong income potential.

6. Useful for Portfolio Investors

DSCR loans are well-suited for investors who are actively building or managing multiple properties. Since qualification is tied to each property individually, investors can continue acquiring additional assets without personal income limitations or traditional debt-to-income restrictions.

This makes DSCR financing a scalable solution for portfolio growth, and investors can expand more efficiently in high-value or cash-flow-driven markets while maintaining flexibility in ownership structure and acquisition strategy.

Cons of DSCR Loans for Investment Properties

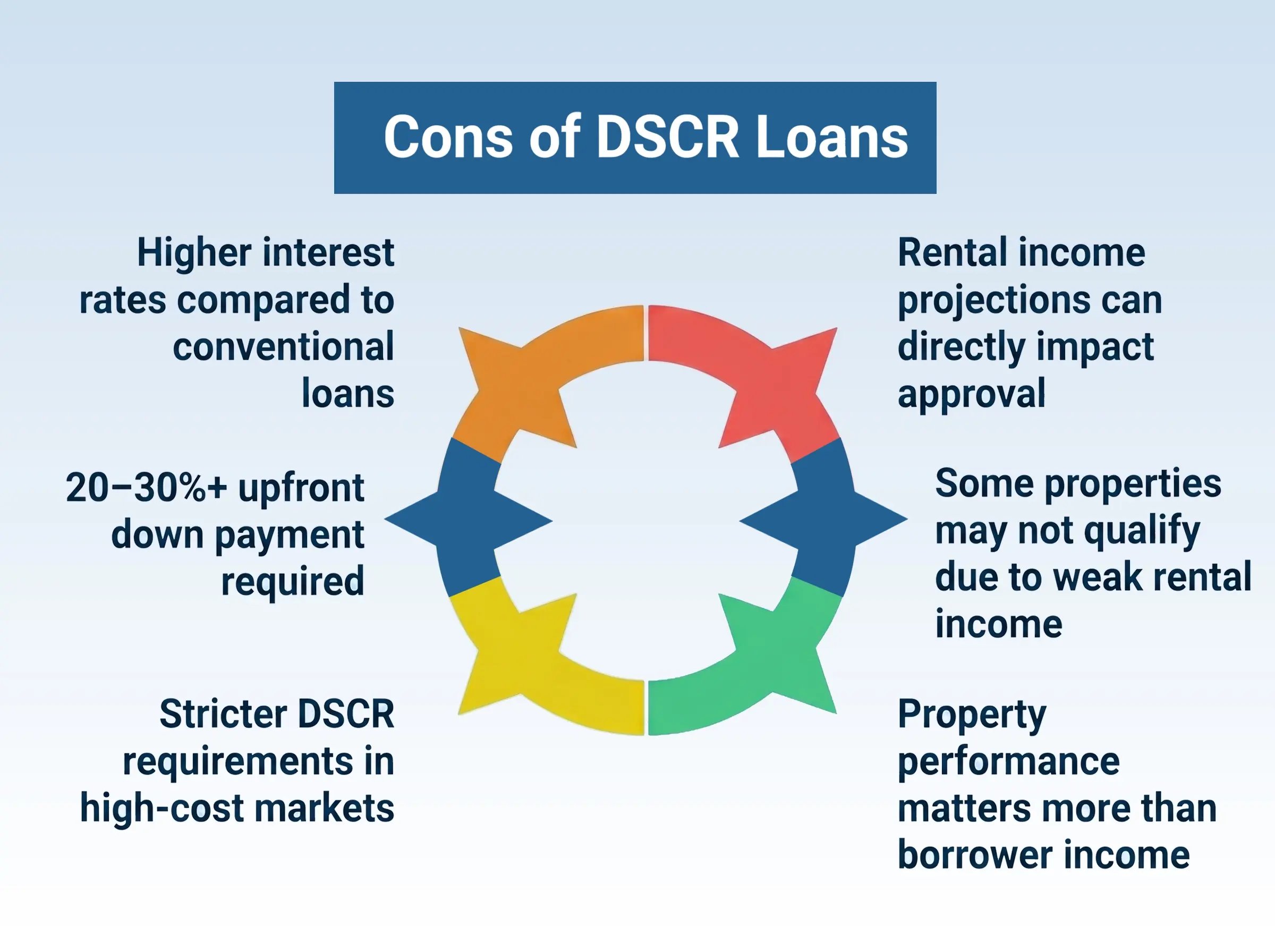

1. Higher Interest Rates on Luxury Properties

Because DSCR loans are considered higher risk, lenders typically charge:

- Higher interest rates than conventional loans

- Stricter pricing on jumbo loans

This can reduce long-term cash flow.

2. Larger Down Payment Requirements

For high-value investment properties, lenders often require:

- 20% to 30%+ down payment

- Sometimes higher for luxury or non-primary residences

This increases upfront capital requirements significantly.

3. Strict DSCR Ratio Requirements in Competitive Markets

In states like California, where property prices are high, lenders may require:

- Stronger DSCR ratios (often 1.2+ preferred)

- Conservative rental income projections

If rental income is weak, approval becomes difficult even if the borrower is financially strong.

4. Property Appraisal and Rental Income Sensitivity

DSCR loan approvals are dependent on the property’s appraised value and its estimated rental income. Lenders typically use market rent reports or appraisal-based rental analysis to determine qualifying income.

If the appraised rent comes in lower than expected, it can directly impact the DSCR ratio and reduce the loan amount or affect approval eligibility.

This makes accurate rent estimation and property selection important, particularly in competitive or rapidly changing rental markets.

5. Risk of Negative Cash Flow in Premium Markets

In expensive markets such as California, property prices can sometimes outpace rental income, which may result in lower DSCR ratios.

Loans can still be closed at DSCR levels as low as 0.75 in some cases; these scenarios typically come with higher interest rates and less favorable pricing compared to stronger DSCR profiles (1.0 and above).

6. Property Performance Matters More Than Borrower Strength

Even if the borrower has excellent credit and assets, DSCR loans depend primarily on:

- Rental income stability

- Market rent accuracy

- Occupancy assumptions

This can be limiting compared to traditional loans.

Why Investors Prefer DSCR Loans

Unlike conventional mortgages, DSCR loans are designed specifically for real estate investors and offer key advantages:

- No income documentation required, no W-2s, pay stubs, or tax returns

- Approval based on property cash flow, not personal debt-to-income (DTI)

- Flexible ownership structures that can be used with LLCs, corporations, or personal names

- Works across multiple property types, including single-family homes, multi-family units, condos, and vacation rentals

- Faster, more flexible underwriting built for investment speed

If you’re an investor focused on scaling your portfolio or purchasing high-value rental properties, DSCR loans provide a financing path built around the performance of the asset, not your employment profile.

At LendFriend, we help you qualify DSCR loans based on your property's rental income and market performance. Our network of investor-friendly lenders makes it easy to qualify, whether you’re financing a duplex in Dallas or an Airbnb in Austin.

Who Should Use a DSCR Loan?

DSCR loans are particularly beneficial for self-employed investors, entrepreneurs, and high-net-worth individuals who may not have traditional income documentation such as W-2s or consistent tax returns.

Since conventional mortgage lending relies heavily on income verification and debt-to-income (DTI) ratios, many qualified investors often face unnecessary hurdles when trying to finance investment properties.

DSCR loans solve this problem by shifting the focus entirely to the property’s rental performance, making it easier to secure financing based on real cash flow rather than personal income structure.

Ideal for Investors Scaling in High-Value Markets

These loans are also a strong fit for investors looking to expand their portfolios quickly without being limited by personal income caps or complex underwriting requirements. Instead of slowing down growth with documentation-heavy approvals, DSCR financing allows investors to move faster in competitive real estate markets.

This is especially valuable when investing in $1M+ properties, where timing and liquidity often play a critical role in securing deals.

Whether you’re purchasing:

- A luxury rental in California

- A high-growth investment property in Texas (Dallas, Austin, Houston)

- Or a cash-flowing rental in Florida’s competitive housing market

DSCR loans provide a scalable financing solution built specifically for investors focused on long-term wealth creation through real estate.

FAQs

What is a good DSCR ratio for loan approval?

Most lenders prefer a DSCR ratio of 1.0 to 1.25 or higher. A ratio above 1.0 means the property generates enough income to cover debt payments. Higher ratios improve approval chances and may result in better loan terms, especially for high-value investment properties.

Who should avoid using a DSCR loan?

DSCR loans may not be suitable for borrowers looking for the lowest possible interest rates, purchasing a primary residence, or investing in properties with weak rental income potential. These loans are best suited for investors focused on cash-flowing rental properties and portfolio growth.

Are DSCR loans a good option for $1M+ investment properties?

DSCR loans can be a strong option for $1M+ properties if the rental income supports the mortgage payments. However, higher loan amounts may come with stricter requirements and higher interest rates.

Final Thoughts: Should You Get a DSCR Loan?

If your goal is to grow a rental portfolio without being restricted by W-2 income or tax returns, then a DSCR loan can be a powerful tool. It allows you to qualify based on the performance of the property rather than your personal financial profile.

However, this flexibility comes at a cost. Higher interest rates, larger down payments, and strict cash-flow requirements mean DSCR loans are only effective when the property is truly income-producing, not borderline or speculative.

If the rental income is strong, DSCR financing can increase your real estate growth. If it is not, the structure can become a long-term cash flow burden.

Schedule a call today or get in touch by completing this quick form, and we'll help you start building your real estate empire.