Author: Eric Bernstein

Author: Eric BernsteinPublished:

Well... we certainly got our first big splash of 2025, but it wasn't what we wanted. The jobs week ended up a dud for homebuyers as reporting was better than expected. Mortgage rates lifted above 7% for the first time since May 2024.

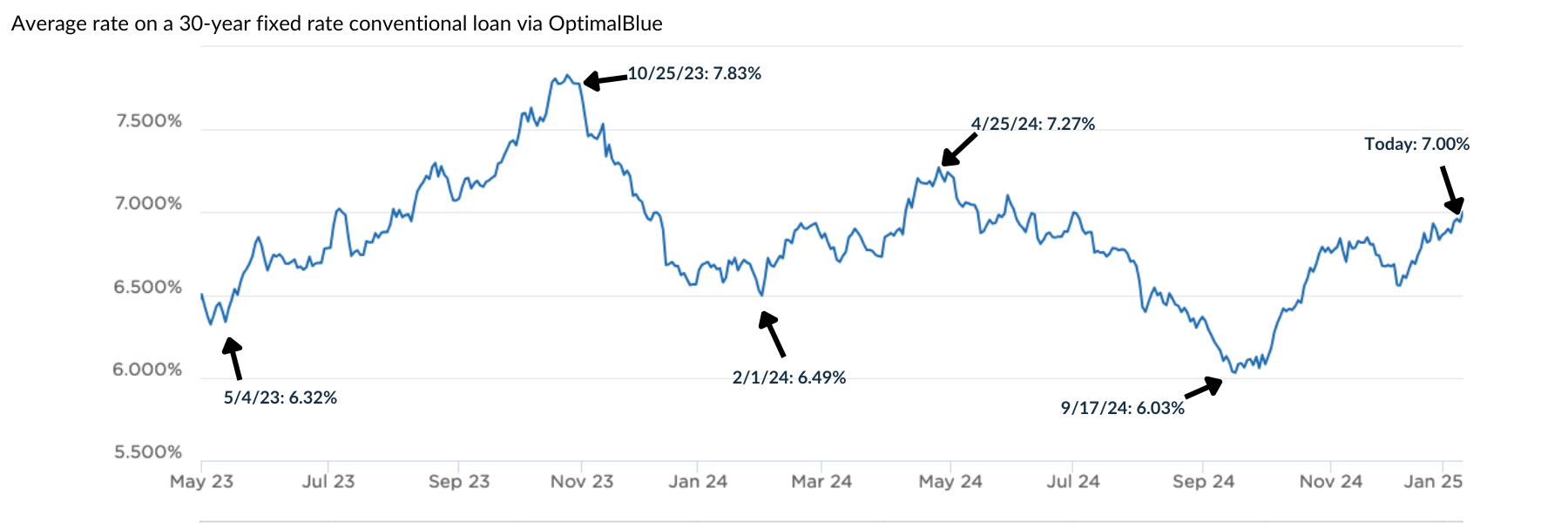

We seem to be in what I'm calling the Rollercoaster Pattern. Instead of getting a trend of mortgage rates heading straight down, we're seeing them hit peaks and valleys every few months, with lower peaks and, hopefully, lower valleys too.

Before I get into the reporting from last week, take a look at the graph below that I made highlighting the Rollercoaster Pattern. You'll see that the peaks and valleys are just a few months from each other, and we've been in this pattern for the last 2 years. Readers of this newsletter will remember that we went through this exact same pain we're feeling today as unrealistically positive jobs data came in over Q1 2024. When the jobs market data was less glowing (or even negative) in Q2 and Q3 we saw rates fall FAST. Homebuyers who bought before Q2 2024 were able to refinance, and in some cases, our client were able to save over $1,000 a month on a refinance.

This is all to say that while the average rate on a 30-year fixed rate conventional loan is at 7.0%, based on the past 2 years of data, we appear to be nearing the top - if we aren't already there. Inflation data coming out this Wednesday and retail data on Thursday will be CRITICAL for mortgage rates. Worse than expected data would mean the Fed is now losing on both fronts of its dual mandate (employment and inflation), which no one wants to see.

Sign up for our weekly Friday rate texts to see all the great options LendFriend provides to homebuyers! One buyer just locked in a 6.5% rate on Friday!

We seem to be in what I'm calling the Rollercoaster Pattern. Instead of getting a trend of mortgage rates heading straight down, we're seeing them hit peaks and valleys every few months, with lower peaks and, hopefully, lower valleys too.

Before I get into the reporting from last week, take a look at the graph below that I made highlighting the Rollercoaster Pattern. You'll see that the peaks and valleys are just a few months from each other, and we've been in this pattern for the last 2 years. Readers of this newsletter will remember that we went through this exact same pain we're feeling today as unrealistically positive jobs data came in over Q1 2024. When the jobs market data was less glowing (or even negative) in Q2 and Q3 we saw rates fall FAST. Homebuyers who bought before Q2 2024 were able to refinance, and in some cases, our client were able to save over $1,000 a month on a refinance.

This is all to say that while the average rate on a 30-year fixed rate conventional loan is at 7.0%, based on the past 2 years of data, we appear to be nearing the top - if we aren't already there. Inflation data coming out this Wednesday and retail data on Thursday will be CRITICAL for mortgage rates. Worse than expected data would mean the Fed is now losing on both fronts of its dual mandate (employment and inflation), which no one wants to see.

Sign up for our weekly Friday rate texts to see all the great options LendFriend provides to homebuyers! One buyer just locked in a 6.5% rate on Friday!

Jobs Data Turns Heads

Jobs Data went from bad to seemingly amazing overnight - off the heels of October and November reporting showing a very cool labor market.

Remember the Fed wants to see a cool labor market because a hot labor market will lead to inflation as competition to hire leads companies to pay workers higher wages (how dare they), leading to higher demand for goods now that more people have more money and higher prices.

- Job Openings grew to 8.1M in November (way more than the 7.7M expected and back above the 8M threshold that no one wants to see). Hirings again slowed - jobs are being added but no one is being hired for the position. Employers added 180,000 jobs a month in 2024 through November, down a fair amount from 251,000 in 2023.

- Private payrolls growth was less than expected again in December. Companies added just 122k jobs on the month, and less than the Dow Jones estimate for 140,000. Interesting, ADP Chief Economist Nela Richardson said "The labor market downshifted to a more modest pace of growth in the final month of 2024, with a slowdown in both hiring and pay gains." While this might have been correct for the data in ADP's hands, it's not what the Labor Department said the very next day....

- Both the stock and bond market was dealt a heavy blow when the Jobs Report came out on Friday showing not on a massive beat on jobs added but a DROP in the unemployment rate. Nonfarm payrolls increased by 256k (above the 155k expected). Worse is that unemployment ticked down to 4.1% (below the 4.2% expected by the market. I think everyone would like to see unemployment closer to 5% and after hitting 4.3% in July 2024 - there was hope that we were on the right track. However, we've been backsliding and that's causing mortgage rates to also backslide to it's prior peak.

When's the next rate cut?

Let's just say that you shouldn't hold your breath. After Friday's jobs report, traders have pushed back their expectations for the next rate cut. Many believe we won't see a rate cut this year until OCTOBER.

But, there's good news! We don't need a rate cut for rates to fall. Remember from April 2024 to September 2024 rates fell 1.24% and there wasn't a single rate cut. As long as we start getting new data that supports either a cooler economy, cooler labor market OR cooler inflation - we will see rates fall, guaranteed.

Key reporting dates this week:

Mon, 1/13: Monthly U.S. federal budget

Tues, 1/14: Producer price index, Core PPI, Fed Beige Book

Wed, 1/15: Consumer price index, Core CPI, Empire State manufacturing survey

Thurs, 1/16: Initial jobless claims, U.S. retail sales, Import price index, Homebuilder confidence

Fri, 1/17: Housing starts, Building permits

.png?width=1200&height=244&name=Homebuyer%20Tools%20Header%20(10).png)

About the Author:

Eric Bernstein is the President and Co-Founder of LendFriend Mortgage, where he helps homebuyers make smarter, more confident decisions in today’s fast-moving housing market. With over a decade of experience guiding hundreds of clients—from first-time buyers to seasoned investors—Eric brings a mix of market insight, strategy, and personalized service to every mortgage transaction. Each week, Eric breaks down the housing and economic headlines that matter, giving readers a clear, no-fluff view of what’s happening and how it might impact their buying power.