Author: Eric Bernstein

Author: Eric BernsteinPublished:

Last week was a relatively uneventful week for interest rates.

While inflation news came in better than expected, the stock market continued to get pummeled as the stock market continues to digest a slower economy and the potential for a recession.

The average rate on a 30-year fixed rate conventional loan stayed flat 6.61% - but our clients are still securing rates as low as 5.99%! Sign up for our weekly Friday rate texts to stay in the know on where rates are week by week! It's a must for anyone planning to buy or refinance in 2025!

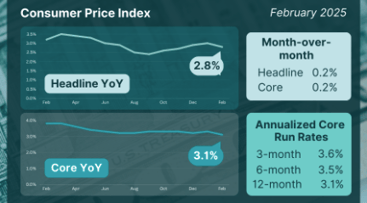

Inflation Is Back On Track

Consumer Price Index (CPI) reported last week and it was an overall better than expected - especially for core CPI. The core CPI, which excludes food and gas prices, rose 0.2% on the month and was at 3.1% on a 12-month basis, the lowest reading since April 2021. Overall CPI was at 2.8% on a 12-month basis (vs. 2.9% expected).

EVERY inflation report feels like a life or death situation for mortgage rates because Powell is at his wits end waiting for inflation to get back down to 2%. We need momentum downward for Powell to get back to cutting rates (or the labor market and economy to fall off a cliff).

“A lot of this inflation data does not incorporate what is to come and what already has happened for tariffs,” said Kevin Gordon, senior investment strategist at Charles Schwab. “The vagaries and uncertainties associated with policy are still a much stronger force in the market than anything CPI-related or in terms of one data point.”

He's right. Tariffs continue to make headlines, causing market uncertainty and consumer confusion. Some of these tariffs affect the price of homebuilding materials which in turn could increase the price of homes (something no one wants to hear).

Consumers are Exhausted

In February, consumer confidence — which can help to signal how much shoppers are willing to shell out — saw the biggest drop since 2021. The Conference Board’s Consumer Confidence Index slipped to 98.3 for the month, down nearly 7% and below the Dow Jones forecast for 102.3.

These numbers might as well be gibberish to me unless you look at it from a multi-year perspective. We've seen consumer confidence fall into 90s in multiple instances in 2022, 2023 and 2024. Is this time different?

Some people think so . There may some type of snowball effect. Wage growth hasn't been as hot in recent years, while inflation and high interest rates have. Consumer credit is at an all time high, and perhaps most importantly, no one can predict how these tariffs are going to impact their wallet. WSJ had an amazing headline "Consumers Keep Bailing Out the Economy. Now They Might Be Maxed Out."

All of this is actually GOOD news for rates as a volatile market with lower consumer spending, will equal lower inflation and more rate cuts. If you recall, the last 2 times we saw rates dip to the lowest of lows were following 2 big recessions (2008 and 2020) and both times, the economy was fine in the long term and those who owned houses enjoyed significant appreciation for years to come.

Fed Meeting Predictions

Another key Fed meeting takes place this Wednesday. While the market currently predicts a 99% chance that rates remain the same, we just never know.

More important than what the Fed decides to do with rates this week - we'll get a bunch of insight on what the Fed is thinking with respect to the state of the economy and where interest rates will be in the future when Powell speaks on Wednesday at 2:30PM ET. Either way, expect a big reaction from the market when Powell takes the mic.

June 18th is still the near certain date for the first rate cut,.

While inflation news came in better than expected, the stock market continued to get pummeled as the stock market continues to digest a slower economy and the potential for a recession.

The average rate on a 30-year fixed rate conventional loan stayed flat 6.61% - but our clients are still securing rates as low as 5.99%! Sign up for our weekly Friday rate texts to stay in the know on where rates are week by week! It's a must for anyone planning to buy or refinance in 2025!

Inflation Is Back On Track

Consumer Price Index (CPI) reported last week and it was an overall better than expected - especially for core CPI. The core CPI, which excludes food and gas prices, rose 0.2% on the month and was at 3.1% on a 12-month basis, the lowest reading since April 2021. Overall CPI was at 2.8% on a 12-month basis (vs. 2.9% expected).

EVERY inflation report feels like a life or death situation for mortgage rates because Powell is at his wits end waiting for inflation to get back down to 2%. We need momentum downward for Powell to get back to cutting rates (or the labor market and economy to fall off a cliff).

“A lot of this inflation data does not incorporate what is to come and what already has happened for tariffs,” said Kevin Gordon, senior investment strategist at Charles Schwab. “The vagaries and uncertainties associated with policy are still a much stronger force in the market than anything CPI-related or in terms of one data point.”

He's right. Tariffs continue to make headlines, causing market uncertainty and consumer confusion. Some of these tariffs affect the price of homebuilding materials which in turn could increase the price of homes (something no one wants to hear).

Consumers are Exhausted

In February, consumer confidence — which can help to signal how much shoppers are willing to shell out — saw the biggest drop since 2021. The Conference Board’s Consumer Confidence Index slipped to 98.3 for the month, down nearly 7% and below the Dow Jones forecast for 102.3.

These numbers might as well be gibberish to me unless you look at it from a multi-year perspective. We've seen consumer confidence fall into 90s in multiple instances in 2022, 2023 and 2024. Is this time different?

Some people think so . There may some type of snowball effect. Wage growth hasn't been as hot in recent years, while inflation and high interest rates have. Consumer credit is at an all time high, and perhaps most importantly, no one can predict how these tariffs are going to impact their wallet. WSJ had an amazing headline "Consumers Keep Bailing Out the Economy. Now They Might Be Maxed Out."

All of this is actually GOOD news for rates as a volatile market with lower consumer spending, will equal lower inflation and more rate cuts. If you recall, the last 2 times we saw rates dip to the lowest of lows were following 2 big recessions (2008 and 2020) and both times, the economy was fine in the long term and those who owned houses enjoyed significant appreciation for years to come.

Fed Meeting Predictions

Another key Fed meeting takes place this Wednesday. While the market currently predicts a 99% chance that rates remain the same, we just never know.

More important than what the Fed decides to do with rates this week - we'll get a bunch of insight on what the Fed is thinking with respect to the state of the economy and where interest rates will be in the future when Powell speaks on Wednesday at 2:30PM ET. Either way, expect a big reaction from the market when Powell takes the mic.

June 18th is still the near certain date for the first rate cut,.

Key reporting dates this week:

Mon, 3/17: U.S. retail sales, Empire State manufacturing survey, Home builder confidence index, Business Inventories

Tues, 3/18: Housing starts, Building permits, Import price index

Wed, 3/19: Fed Meeting, Fed Chair Powell press conference

Thurs, 3/20: Initial jobless claims, Existing home sales

Fri, 3/21: None scheduled

.png?width=1200&height=244&name=Homebuyer%20Tools%20Header%20(10).png)

About the Author:

Eric Bernstein is the President and Co-Founder of LendFriend Mortgage, where he helps homebuyers make smarter, more confident decisions in today’s fast-moving housing market. With over a decade of experience guiding hundreds of clients—from first-time buyers to seasoned investors—Eric brings a mix of market insight, strategy, and personalized service to every mortgage transaction. Each week, Eric breaks down the housing and economic headlines that matter, giving readers a clear, no-fluff view of what’s happening and how it might impact their buying power.