Author: Eric Bernstein

Author: Eric BernsteinPublished:

Homebuyers experienced their first big wins of 2025 when inflation came in better than expected while retail sales came in worse than expected. The 1-2 punch sent mortgage rates tumbling.

The average rate on a 30-year fixed rate conventional loan fell by almost 1/8th of a percent to 6.91% (down from 7.01%), which is a HUGE 1 week drop. Was my bold prediction that we saw the top of mortgage rates last week right?! I hope so!

With Trump's presidency starting yesterday, anything can happen as a new administration with a whole new approach takes the reigns on how to handle the U.S. economy.

If you haven't yet, sign up for our weekly Friday rate texts to stay in the know on where rates are week by week! It's a must for anyone planning to buy or refinance in 2025!

The Market LOVED the Inflation Reports

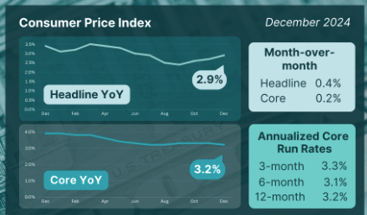

The December Consumer Price Index (CPI) report was so good for homebuyers that it erased all the negative impacts from the December Jobs Report and then some. So, why was it so good?

First, top line CPI came in right at expectations and when the labor market was looking as hot as it was the week prior and there's tons of articles discussing the resilience of consumers, there was significant concern that the top line would be above expectation.

Next, core CPI was LOWER than expectations (3.2% actual vs 3.3% expected). We've been oscillating between 3.2 and 3.3% since roughly July 2024 (before the Fed's first rate cut) and seeing it heading down after 3 rate cuts PLUS hot labor reporting is welcome relief. Maybe the Fed didn't cut too much after all....

Finally, shelter costs! If you recall, I've been harping on shelter costs for well over a year. Stubbornly high shelter costs, which make up 1/3 of the CPI, hasn't given us any relief. But finally, we're seeing a crack in the armor. Shelter costs rose just 4.6% from a year ago, which I know sounds like a lot but it's actually the smallest one-year gain since January 2022! For reference, shelter costs peaked in March 2023 at 8.16% year over year growth and has steadily (but way too slowly) been falling. Pre-pandemic levels were roughly 3-3.5% in any given month.

Overall a great report, and both bond and stock markets reacted positively - which led to sharply lower mortgage rates on the day.

Retail Sales Disappointed

Retail sales weren't as strong as investors hoped in December (0.4% increase (actual) vs 0.6% increase (expected)). Investors wanted to see unbelievable spending this holiday season and unfortunately, it just didn't happen. It's another sign that maybe the economy isn't as rosy as many believed it to be after the December Jobs Report and another reason for mortgage rates to head lower. And they did.

When's the next rate cut?

On 1/17, most analysts believed we wouldn't see another rate cut until October. Just 1 week later, over 50% of polled analysts believe we'll see another rate cut on May 7th! Better than the initially predicted date of June 18th!

That just goes to show you how much can change with a few key reports. One week we are on track (or ahead of schedule) for a rate cut and the next week we could be facing major delays.

Richmond Fed President Thomas Barkin stated that the December CPI report "continues the story we have been on, which is that inflation is coming down towards target."

New York Fed President John Williams said "The process of disinflation remains in train," however, with respect to the upcoming Trump presidency, "the economic outlook remains highly uncertain, especially around potential fiscal, trade, immigration, and regulatory policies." Seeing Trump's policies begin to unfold under the next few months may have a heavy influence the Fed's next step.

It's a VERY light news week this week (other than President Trump's inauguration yesterday).

The average rate on a 30-year fixed rate conventional loan fell by almost 1/8th of a percent to 6.91% (down from 7.01%), which is a HUGE 1 week drop. Was my bold prediction that we saw the top of mortgage rates last week right?! I hope so!

With Trump's presidency starting yesterday, anything can happen as a new administration with a whole new approach takes the reigns on how to handle the U.S. economy.

If you haven't yet, sign up for our weekly Friday rate texts to stay in the know on where rates are week by week! It's a must for anyone planning to buy or refinance in 2025!

The Market LOVED the Inflation Reports

The December Consumer Price Index (CPI) report was so good for homebuyers that it erased all the negative impacts from the December Jobs Report and then some. So, why was it so good?

First, top line CPI came in right at expectations and when the labor market was looking as hot as it was the week prior and there's tons of articles discussing the resilience of consumers, there was significant concern that the top line would be above expectation.

Next, core CPI was LOWER than expectations (3.2% actual vs 3.3% expected). We've been oscillating between 3.2 and 3.3% since roughly July 2024 (before the Fed's first rate cut) and seeing it heading down after 3 rate cuts PLUS hot labor reporting is welcome relief. Maybe the Fed didn't cut too much after all....

Finally, shelter costs! If you recall, I've been harping on shelter costs for well over a year. Stubbornly high shelter costs, which make up 1/3 of the CPI, hasn't given us any relief. But finally, we're seeing a crack in the armor. Shelter costs rose just 4.6% from a year ago, which I know sounds like a lot but it's actually the smallest one-year gain since January 2022! For reference, shelter costs peaked in March 2023 at 8.16% year over year growth and has steadily (but way too slowly) been falling. Pre-pandemic levels were roughly 3-3.5% in any given month.

Overall a great report, and both bond and stock markets reacted positively - which led to sharply lower mortgage rates on the day.

Retail Sales Disappointed

Retail sales weren't as strong as investors hoped in December (0.4% increase (actual) vs 0.6% increase (expected)). Investors wanted to see unbelievable spending this holiday season and unfortunately, it just didn't happen. It's another sign that maybe the economy isn't as rosy as many believed it to be after the December Jobs Report and another reason for mortgage rates to head lower. And they did.

When's the next rate cut?

On 1/17, most analysts believed we wouldn't see another rate cut until October. Just 1 week later, over 50% of polled analysts believe we'll see another rate cut on May 7th! Better than the initially predicted date of June 18th!

That just goes to show you how much can change with a few key reports. One week we are on track (or ahead of schedule) for a rate cut and the next week we could be facing major delays.

Richmond Fed President Thomas Barkin stated that the December CPI report "continues the story we have been on, which is that inflation is coming down towards target."

New York Fed President John Williams said "The process of disinflation remains in train," however, with respect to the upcoming Trump presidency, "the economic outlook remains highly uncertain, especially around potential fiscal, trade, immigration, and regulatory policies." Seeing Trump's policies begin to unfold under the next few months may have a heavy influence the Fed's next step.

It's a VERY light news week this week (other than President Trump's inauguration yesterday).

Key reporting dates this week:

Mon, 1/20: MLK Jr. Day

Tues, 1/21: None Scheduled

Wed, 1/22:U.S. leading economic indicators

Thurs, 1/23: Initial jobless claims

Fri, 1/24: Existing home sales

.png?width=1200&height=244&name=Homebuyer%20Tools%20Header%20(10).png)

About the Author:

Eric Bernstein is the President and Co-Founder of LendFriend Mortgage, where he helps homebuyers make smarter, more confident decisions in today’s fast-moving housing market. With over a decade of experience guiding hundreds of clients—from first-time buyers to seasoned investors—Eric brings a mix of market insight, strategy, and personalized service to every mortgage transaction. Each week, Eric breaks down the housing and economic headlines that matter, giving readers a clear, no-fluff view of what’s happening and how it might impact their buying power.