Author: Eric Bernstein

Author: Eric BernsteinPublished:

This past week was a very interesting one for the housing market. Interest rates held mostly flat as out-of-control government spending was balanced out from reports of very little spending by consumers.

As expected, the housing market remains "frozen" as millions of Americans and foreign investors are waiting for lower interest rates - but home prices keep heading higher - even in this high interest rate environment.

The average rate on a 30-year fixed rate conventional loan held steady at 6.85% (very slightly up from the 6.83% I reported last week).

As expected, the housing market remains "frozen" as millions of Americans and foreign investors are waiting for lower interest rates - but home prices keep heading higher - even in this high interest rate environment.

The average rate on a 30-year fixed rate conventional loan held steady at 6.85% (very slightly up from the 6.83% I reported last week).

Make sure you're signed up for our weekly Friday rate texts. It could make a HUGE difference in your homebuying decision.

A Tale of Two Spenders

A Tale of Two Spenders

It's the government vs. consumers, and it looks like the government has much deeper pockets (but who is footing the bill? 🤔)

Last week we found out that the government is on track to hit a nearly $2 TRILLION budget gap (up 27% from 2023's spending deficit of $1.69 trillion). The top reasons for the widening gap are foreign aid, student debt relief, medicare costs and payments to cover bank failures in 2023 and 2024 😲.

Meanwhile, consumers are tapping out. Retail sales in May came in lower than expected of (0.1% actual vs 0.2% expected) and, even worse, April retail sales data revised down from flat to a drop of 0.2%.

Why is this important for homebuyers?

Heavy government spending is BAD for homebuyers. Economists believe that the larger the US deficit becomes, the higher the interest rate on government bonds will be because the risk of default goes up. Mortgage rates and government bonds are closely tied together so any increase in government bond interest rates will increase mortgage rates.

Meanwhile, bad consumer spending is GOOD for homebuyers. The less consumers spend, the lower inflation will be. GDP will fall as consumer spending makes up a BIG chunk of GDP plus retailers will be encouraged to reduce prices and layoff unnecessary workforce to compensate for lower demand - all of which will encourage the Fed to cut rates sooner.

Existing Home Sales Fall Again

Exiting home sales fell for the THIRD month in a row. Falling 2.8% compared with May last year and 0.7% from last month - that's a pace of 4.11 million homes expected to sell this year, which is actually slightly higher than the 4.07 million pace economists were expecting, according to FactSet.

This pace of sales isn't nearly as slow as we saw it at some points in 2023, but mortgage rates and high home prices are still keeping many buyers and potential sellers on the sidelines.

Even crazier, despite the slow housing market we've seen for years now, home prices keep climbing. Nationwide home prices are up 5.8%!!!

The one piece of good news for those who haven't bought yet is that inventory is growing SLOWLY. Over the last year nationwide inventory has gone from 990,000 homes to 1.28M homes (which is 3.7 months of supply). Economists would like to see this number at or above 2M before we can officially declare this seller's market to be over.

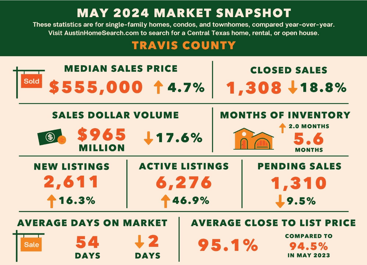

But ALWAYS keep in mind - real estate is local. Nationwide inventory can vary widely from your local area. In Travis County, inventory is near record highs of at 5.6 months! Meaning, many buyers are experiencing the MOST negotiating power they've ever had. That doesn't mean home prices are falling though. Home prices throughout Travis County are still up 4.7% from last year.

RATE CUT WATCH: Odds on a September rate cut are stable after last week's reporting. There's a 66% chance of a rate cut will take place on September 18th.

Meanwhile, consumers are tapping out. Retail sales in May came in lower than expected of (0.1% actual vs 0.2% expected) and, even worse, April retail sales data revised down from flat to a drop of 0.2%.

Why is this important for homebuyers?

Heavy government spending is BAD for homebuyers. Economists believe that the larger the US deficit becomes, the higher the interest rate on government bonds will be because the risk of default goes up. Mortgage rates and government bonds are closely tied together so any increase in government bond interest rates will increase mortgage rates.

Meanwhile, bad consumer spending is GOOD for homebuyers. The less consumers spend, the lower inflation will be. GDP will fall as consumer spending makes up a BIG chunk of GDP plus retailers will be encouraged to reduce prices and layoff unnecessary workforce to compensate for lower demand - all of which will encourage the Fed to cut rates sooner.

Existing Home Sales Fall Again

Exiting home sales fell for the THIRD month in a row. Falling 2.8% compared with May last year and 0.7% from last month - that's a pace of 4.11 million homes expected to sell this year, which is actually slightly higher than the 4.07 million pace economists were expecting, according to FactSet.

This pace of sales isn't nearly as slow as we saw it at some points in 2023, but mortgage rates and high home prices are still keeping many buyers and potential sellers on the sidelines.

Even crazier, despite the slow housing market we've seen for years now, home prices keep climbing. Nationwide home prices are up 5.8%!!!

The one piece of good news for those who haven't bought yet is that inventory is growing SLOWLY. Over the last year nationwide inventory has gone from 990,000 homes to 1.28M homes (which is 3.7 months of supply). Economists would like to see this number at or above 2M before we can officially declare this seller's market to be over.

But ALWAYS keep in mind - real estate is local. Nationwide inventory can vary widely from your local area. In Travis County, inventory is near record highs of at 5.6 months! Meaning, many buyers are experiencing the MOST negotiating power they've ever had. That doesn't mean home prices are falling though. Home prices throughout Travis County are still up 4.7% from last year.

RATE CUT WATCH: Odds on a September rate cut are stable after last week's reporting. There's a 66% chance of a rate cut will take place on September 18th.

PCE Reporting (the Fed's favorite inflation metric) is THIS Friday. Good or bad news will have a BIG impact on rates. Based on the last several months of news, I expect it to be a good report for homebuyers, but in this market, there are no certainties!

Key reporting dates this week:

Mon, 6/24: Fed speakers

Tues, 6/25: S&P Case-Shiller home price index (20 cities), Consumer confidence

Wed, 6/26: New construction home sales

Thurs, 6/27: Initial jobless claims, Pending home sales, GDP (2nd revision)

Fri, 6/28: PCE, Personal spending, Personal income

.png?width=1200&height=244&name=Homebuyer%20Tools%20Header%20(10).png)

About the Author:

Eric Bernstein is the President and Co-Founder of LendFriend Mortgage, where he helps homebuyers make smarter, more confident decisions in today’s fast-moving housing market. With over a decade of experience guiding hundreds of clients—from first-time buyers to seasoned investors—Eric brings a mix of market insight, strategy, and personalized service to every mortgage transaction. Each week, Eric breaks down the housing and economic headlines that matter, giving readers a clear, no-fluff view of what’s happening and how it might impact their buying power.