Author: Michael Bernstein

Author: Michael BernsteinPublished:

Understanding how global trade, inflation, and interest rates intersect isn’t just for economists — it’s essential for anyone thinking about buying a home.

Tariffs are front and center again in 2025 - thanks to Trump's economic agenda. And while they may seem like an abstract part of global politics, they have real consequences for mortgage rates, inflation, and home prices across the country — especially here in Austin.

So what’s happening, and how should you think about your next move in this market? Let’s break it down.

Trump's ‘Beautiful’ Tariffs Are Back — But the World Has Changed

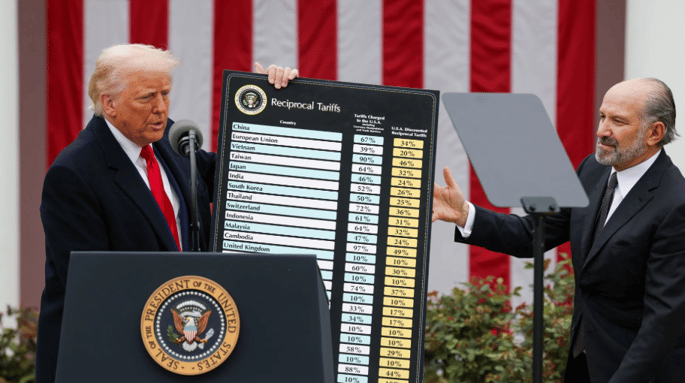

President Trump has made no secret of his admiration for tariffs. In his view, they’re a powerful tool to bring manufacturing back home and strengthen American industries — a throwback to a 1950s-style economic dominance. In 2025, that philosophy has returned with full force, and it’s reshaping global trade in real time.

Over the last few months, we’ve seen sweeping tariffs reimposed on goods from China, Japan, South Korea, and Canada. China alone was hit with a staggering 145% tariff on certain imports earlier this year — now temporarily reduced to 30% as part of a short-term “cooling off” agreement. But the progress is minimal: most of the trade barriers remain firmly in place. Canada and Japan are still facing tariffs on key exports. South Korea is pushing back in international courts. And even with the UK, where a deal seemed within reach, only modest exemptions have been secured.

Despite all this, the average consumer hasn’t seen a huge difference yet. But the pressure is building. These tariffs function like taxes on imported goods — whether it’s appliances, building materials, or car parts — and those costs don’t vanish. They trickle down to consumers and builders, especially in industries like real estate where material costs are critical.

Why Mortgage Rates Haven’t Fallen

At the same time, the stock market has been on a tear after the big drop we saw following Trump's Liberation Day announcement of reciprocal tariffs. In large part it's because the stock market believes these tariffs will not affect long term economic growth. Normally, that kind of bullish momentum we see in the stock market because of lessening tariff fears could lead to lower mortgage rates, as investors move money out of bonds and into stocks.

But not this time.

Why? Because the bond market — and the Federal Reserve — are still laser-focused on inflation.

Even with cooling CPI data earlier this month, Federal Reserve Chair Jerome Powell has made it clear: he’s not ready to cut rates yet. In fact, he’s openly stated that the full effects of tariffs on inflation haven’t even shown up in the data yet. Until they do — and unless they’re mild — the Fed is holding tight.

That’s why we’re still seeing mortgage rates hover just above 7%, the highest since February. The market knows that inflationary pressure from tariffs is real, and the Fed is being intentionally cautious.

Powell vs. Trump: A Delicate Dance

The dynamic between President Trump and Federal Reserve Chair Jerome Powell has become a focal point in 2025's economic narrative. The President advocates for aggressive economic policies and wants ultra low rates to come back to help with expansive growth. Powell and the Fed, on the other hand, are exercising caution. Their primary concern: the potential inflationary impact of these tariffs and the broader implications for the U.S. economy.

At the May 7 Federal Reserve press conference, Powell emphasized, "If the large increases in tariffs that have been announced are sustained, they are likely to generate a rise in inflation, a slowdown in economic growth, and an increase in unemployment." While this statement came just before the US-China temporary truce was announced on 5/11, it underscores the Fed's concern that prolonged trade tensions could lead to stagflation—a combination of stagnant economic growth and high inflation.

Despite President Trump's public calls for immediate rate cuts, Powell maintained the Fed's independence, asserting that such political pressures do not influence the central bank's decisions. "Our obligation is to keep longer-term inflation expectations well anchored and to prevent a one-time increase in the price level from becoming an ongoing inflation problem." (aka our obligation is not to Trump's agenda).

For prospective homebuyers, this ongoing tension between the administration's trade policies and the Fed's cautious approach means that mortgage rates may remain elevated in the near term.

Tariffs Could Actually Push Home Prices Higher

Here’s what most people miss: tariffs don’t just affect your rate — they also affect your price.

If it costs more to build, renovate, or furnish a home, those costs get passed on. We’re already seeing developers in Austin revise budgets upward for 2025 builds, citing higher lumber, appliance, and HVAC costs tied to trade restrictions. When supply stays tight and construction gets more expensive, what happens next? Prices go up.

That’s why waiting for prices to “come down” could be a risky bet. Even if rates soften later this year, higher home prices may erase much of the benefit.

Bottom Line: Don’t Wait for a Perfect Market

We get it — buying a home right now can feel overwhelming. Rates are high, headlines are noisy, and global events are shifting quickly.

But here’s what we know: even in times of uncertainty, real estate remains one of the most reliable long-term investments you can make. Especially in a growing city like Austin, where population growth and housing demand continue to outpace supply.

And here’s the good news — you don’t have to time the market perfectly. You just have to make a smart decision for where you are right now. With the right financing strategy (and a lender who’s in your corner), you can lock in a home you love and refinance later if rates improve.

If you want to discuss your loan options and how to get the best rate in this economic environment, give us a call at 512.881.5099 or get in touch with me by completing this quick form, and I'll be in touch as soon as possible.